MARK SCHUMANN

Apparently in response to public criticisms by City Councilwoman Pilar Turner, Utility Commission Chairman Scott Stradley, Taxpayer’s Association Treasurer Alice Johnson, pro-sale utility activist Glenn Heran and others, Florida Municipal Power Agency General Manager Nicholas Guarriello released a four-page “fact sheet” yesterday explaining the financing of the FMPA power projects in which Vero Beach is a participant.

In an accompanying letter to City Manager Jim O’Connor, Guarriello indicated comments made in public meetings about the FMPA Stanton I and II and St. Lucie Two projects are “very inaccurate.”

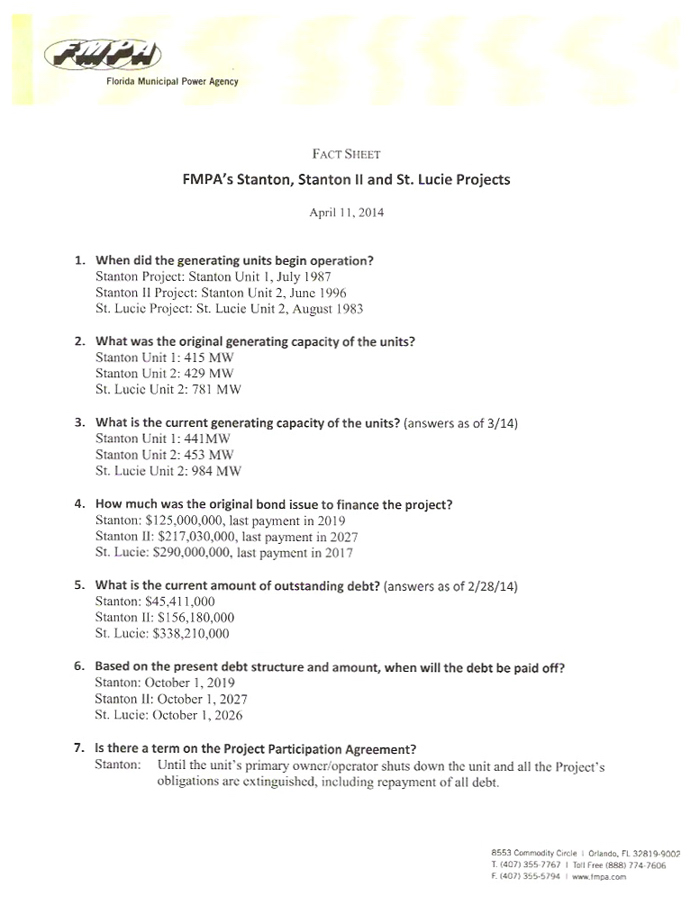

In her presentation to the City Council recently, Turner repeated her assertion that at least one of the projects is financed through 2066. According to Guarriello, based on the present debt structure, the last bond payment will be made in October 2027. Regardless of when the bonds are paid off, though, project participants, such as Vero Beach, are committed until the debt is retired, or for the life of the generating units, whichever comes later.

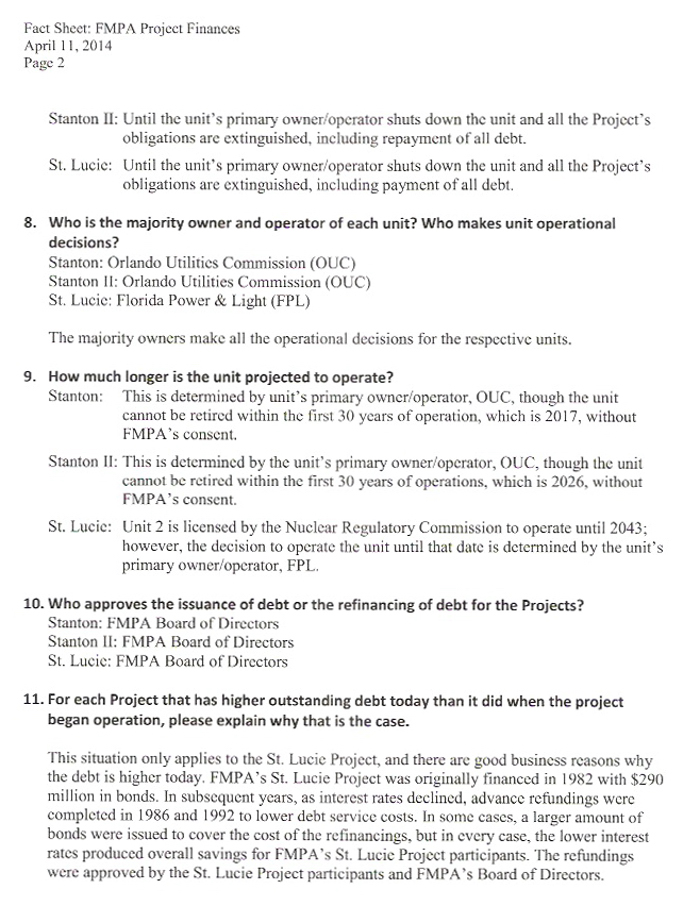

Stradley, Heran and Johnson have all suggested the FMPA is a house of cards. Johnson, for example, came before the City Council March 18 and raised concerns with the FMPA’s balance sheet. She said the debt keeps going up, but the assets are the same. In truth, one of the three FMPA power projects in which Vero Beach participates, St. Lucie Nuclear Unit Two, does have more debt than when the bonds were first issues. The FMPA’s debt on the St. Lucie project is now $338.2 million, up from $290 million when the plant was built. Guarriello explained that the St. Lucie project was refinanced when Florida Power & Light upgraded the plant to increase its generating capacity 26 percent.

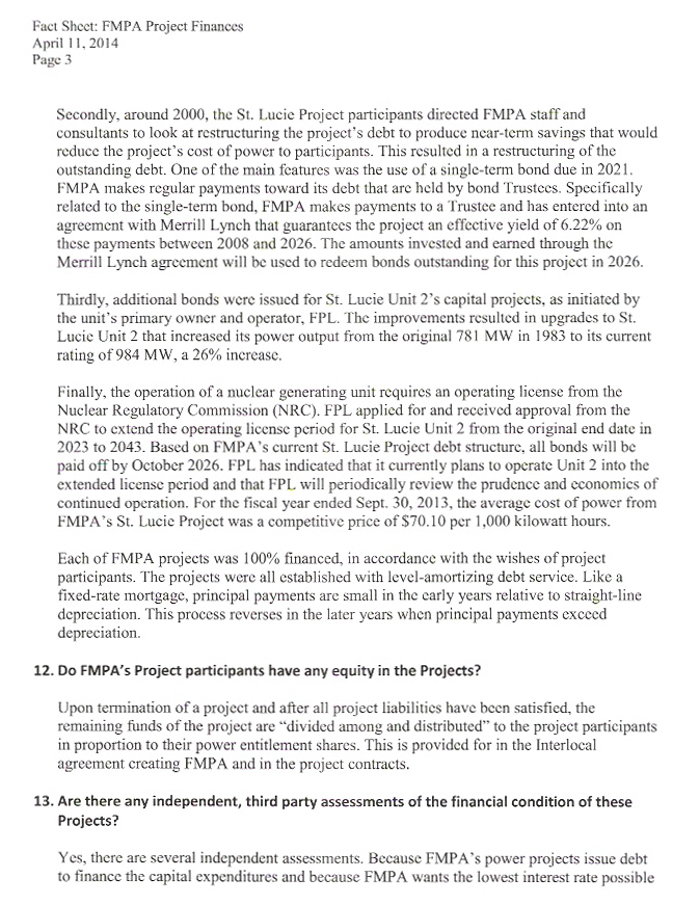

Stradley consistently argues that the FMPA is mismanaged “by utility directors and city managers.” Heran is currently giving a presentation throughout the community positioning the FMPA as a grossly mismanaged organization that is now the cause of all the city’s utility issues. At least half a dozen times during a recent presentation to the Rotary Club of Vero Beach, Heran accused the FMPA of attempting to “strip the city of its assets.” According the the FMPA fact sheet, “Upon termination of a project and after all project liabilities have been satisfied, the remaining funds of the project are divided among and distributed to the project participants in proportion to their power entitlement shares.”

Beyond explaining the status of the financing on the Stanton I and II and St. Lucie Two power projects, Guarriello outlined the independent, three party assessments of the FMPA’s financial condition that are available to investors and the public. In addition to subjecting its financial statements to an independent audit, the FMPA is reviewed by Moody’s Investor Services and Fitch Ratings, two of the largest independent credit rating agency is the world. Both agencies continue to give FMPA’s projects high ratings. See also: Moody’s credit rating service raises cautions about Vero Beach power sale

The following is the full text of the fact sheet issued yesterday on the financing of the FMPA’s Stanton I and II and St. Lucie Two power projects:

As we have seen through this entire sales fiasco, if the facts work against your agenda, just make your “facts” to help out so they fit your agenda.