Meanwhile, Fitch rating agency positive about outlook for Vero Electric, says utility sale is unlikely

COMMENTARY

MARK SCHUMANN

Backed by the usual cast of suspects and interlopers, including Glenn Heran, Steven Faherty, Mark Mucher and Charlie Wilson, Indian River Shores special counsel Bruce May attempted at a mediation session today to make the case that Vero Electric’s rates are “capricious and unreasonable.”

One Shores resident, Ted Robinson, when so far as to accuse the Vero Beach City Council of “price gouging and price fixing.”

Ironically, in a guest column published August 18 in the Gainesville Sun, Florida Power & Light CEO Eric Silagy essentially, though surely unintentionally, made the case that Vero Electric’s rates are at or close to the national average. Vero Electric’s rate is actually lower than a number of Florida’s investor-owned utilities, all of which are charging rates approved by the Florida Public Service Commission. Currently, the statewide average for investor-owned utilities is $124.94 per 1000 kWh, and $122.08 for municipal utilities. Vero Beach’s rate is $123.93.

Sources in the know believe steps the City is pursuing to lower rates, including decommissioning the power plant and renegotiating the City’s wholesale power agreement with the Orlando Utilities Commission, could bring Vero Electric’s rates to within 10 percent of FPL.

The OUC recently cut a five-year deal with the City of Lake Worth for wholesale power at a rate some 25 percent below what Vero Beach is paying under its 20-year agreement with the Orlando-based utility. Lake Worth’s rates are now equal to FPL, allowing for a 6 percent franchise fee.

In complete defiance of established utility law, the Shore’s is arguing its residents have a right to choose a different electric provider and to force Vero Beach to remove its utility infrastructure from within the town, if Vero Electric is not willing or able to match FPL rates. In tandem with the Shores, the Indian River County Commission has essentially asked the PSC for permission to seize Vero Beach’s utility assets and customer base located in the unincorporated areas of the county.

The two sides will meet next Sept. 26. One week later, the PSC is expected to rule on the County’s complaint. Of 56 electric utilities in Florida, 53 have already lined up in opposition to the County.

For all the ranting and raving about rates that went on at the Shores Town Hall today, there was no discussion of a glowing report on Vero Electric recently released by the Fitch rating agency. Among other positive trends, Fitch sited improved attention to rates and a favorable debt profile.

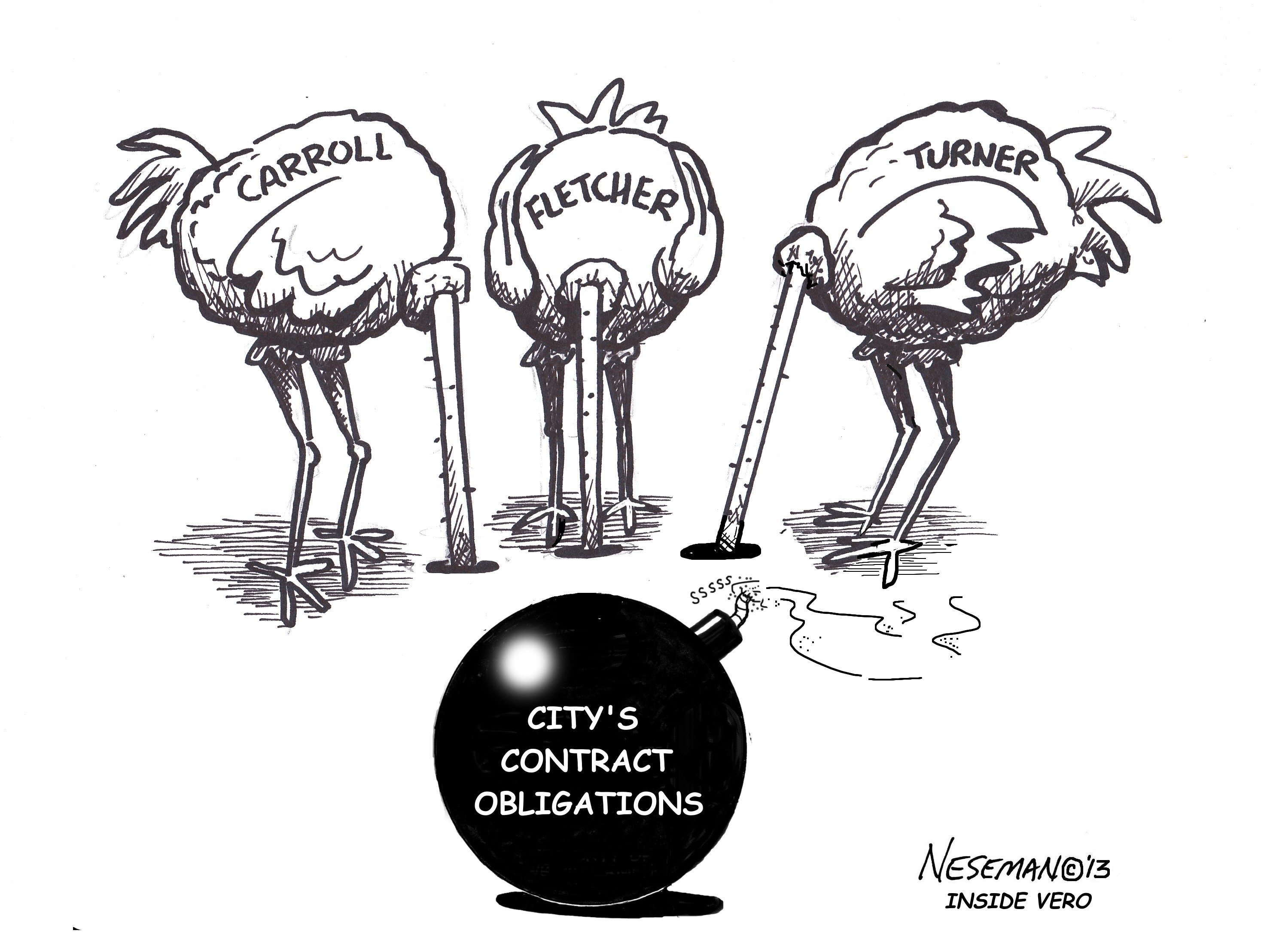

Without offering any specifics, city council candidate, Charlie Wilson, goes before the television cameras at virtually every City Council meeting to accuse current City leaders of “taking the sale from a done deal to a dead deal.” In truth, since Pilar Turner and Craig Fletcher lost Tracy Carroll’s support and became a minority on the Council, insurmountable legal impediments to the sale became undeniable, even by those with their heads buried in the sand.

The Carroll-Fletcher-Turner troika managed Vero Electric by benign neglect. They failed to consider alternatives to a sale, incurred $1.5 million in legal fees on a flawed sales contract before addressing the City’s major contractual obligations and made no serious effort to lower rates. In stark contract, the current City Council has initiated management controlled and has lowered rates, all moves applauded by Fitch analysts.

BusinessWire.com reported, “Since Fitch’s last review, the sale of the city’s electric system to FPL has encountered fairly insurmountable obstacles and now appears unlikely to occur.”

Below is the full report posted August 18 on BusinessWire.com:

NEW YORK– (BUSINESS WIRE)–Fitch Ratings affirms the City of Vero Beach’s, $39.9 million in electric refunding revenue bonds (series 2003A) at ‘A+’.

The Rating Outlook is Stable.

SECURITY

The bonds are secured by the net revenues derived by the city solely from the operation of its electric system.

KEY RATING DRIVERS

SMALL ELECTRIC UTILITY SYSTEM: Vero Beach’s electric utility provides retail service to a relatively small, but stable service area with somewhat below average demographics. Energy sales had been declining since 2011, but exhibited modest growth in 2014.

ADEQUATE POWER SUPPLY: Favorable wholesale contracts together with city-owned generation units provide sufficient resources to meet energy and capacity needs for the foreseeable future.

SOLID FINANCIAL METRICS: Coverage ratios have improved since 2011, despite lower kwh sales thru 2013, largely due to stronger recovery of fuel and purchased power costs. Debt service coverage (DSC) rose to 2.31x in fiscal year (FY) 2013 from 1.88x in FY2011, and typically exceeded 2.4x prior to 2011. Adjusting for purchased power expenses and transfers to the city, Vero Beach’s coverage of full obligations (1.12x) remains slightly below the rating category median (1.37x for 2013).

IMPROVED ATTENTION TO RATES: Over the past two years, management has focused on quarterly review and adjustment of rates to ensure more timely recovery and solidify financial metrics, which Fitch views favorably. Coverage of full obligations should continue to improve in 2015 on improved recovery and a 14.9% decline in debt service.

FAVORABLE DEBT PROFILE: Leverage ratios compare well to medians for the rating category, as the system continues to fund its capital plan from cash flow. Additionally, an outstanding 2008 bank loan was retired in fiscal 2013, boosting equity-to-total capitalization to 71.7% for FY2013. Debt-to-funds available for debt service (FADS), at 2.9x for fiscal 2013 should improve further to about 2.6x in fiscal 2014.

SALE OF THE UTILITY UNLIKELY: The sale of Vero Beach’s electric assets pursuant to an agreement with Florida Power & Light Co. (FP&L; Issuer Default Rating of ‘A’ by Fitch) now appears unlikely to occur, given the challenges of addressing the utility’s interest in Florida Municipal Power Agency (FMPA; rated ‘A+’ by Fitch) generating projects. Nonetheless, Fitch views the proposed sale as credit neutral based on the understanding that any sale would result in either repayment or defeasance of the outstanding series 2003A bonds.

RATING SENSITIVITIES

PENDING RATE AND FINANCIAL FORECAST: Vero Beach plans to update its five year rate and financial forecast (last completed in 2009) by January 2015. Continued improvement in financial performance, together with a keener focus on rate setting and greater certainty of ownership going forward, could warrant consideration of positive Outlook or rating upgrade.

CREDIT PROFILE

The city’s retail electric system serves 34,308 customers in a 40 square mile area. The electric system is a vertically integrated system, with roughly 50% of available capacity attributable to owned gas/oil fired generation units, about 17% in generation entitlements via FMPA; and the rest (approximately 100MW) purchased from Orlando Utilities Commission (rated ‘AA’ by Fitch) via a long term supplemental contract. The system’s wholesale power purchases coupled with its own generating units continue to provide adequate power supply to meet the needs of its customer base for the foreseeable future.

SALE OF ELECTRIC ASSETS TO FLORIDA POWER & LIGHT (FP&L)

Since Fitch’s last review, the sale of the city’s electric system to FP&L has encountered fairly insurmountable obstacles and now appears unlikely to occur. The largest hurdle appears to be finding a mutually and legally acceptable exit strategy (stranded cost issues) in regards to Vero Beach’s entitlement interests in FMPA generation projects. Management has consistently noted that the sale of the electric system would be difficult given the numerous approvals that are needed (including Florida Public Service Commission, Federal Energy Regulatory Commission, Vero Beach City Council, FMPA and OUC).

The Asset Purchase and Sale Agreement with FP&L, which provides for the acquisition of the electric utility assets for approximately $111.5 million does not terminate until Sept. 1, 2016. Fitch will continue to monitor the potential sale of the system, although unlikely at this time.

FINANCIAL PERFORMANCE IS IMPROVING

Financial performance eroded somewhat in fiscal 2011, as a full year of the OUC contract change resulted in a 15% decline in revenues, coupled with kwh sales that were in decline. Positively, financial performance has improved and stabilized since then.

Debt service coverage which peaked at 4.3x in fiscal 2010, declined to 1.88x in fiscal 2011, has rebounded to 2.3x in fiscal 2013. Over the past two years, management has been closely tracking sales, revenues and expenses. Rate and revenue sufficiency is consistently reviewed on a quarterly basis, and rates are adjusted as needed. Liquidity, which dropped in fiscal 2013 to 77 days cash (available cash was used to accelerate paydown of 2008 bank loan) has recovered to 92 days as of the end of third quarter fiscal 2014.

Prospectively, financial metrics should strengthen beginning in 2015. In 2013, management opted to use cash reserves to retire an outstanding bank loan ($3.2 million) to reduce rates going forward. With the $1 million reduction in annual debt service beginning in fiscal 2015 coupled with a return to growth in kwh sales (sales returned to growth through first nine months of fiscal 2014), Fitch estimates Vero Beach’s debt service coverage measures could improve by approximately 30 basis points.

Vero Beach’s financial forecast is expected to be completed in January 2015. Vero Beach’s last capital plan included $15.3 million in expenditures through fiscal 2019. Planned investment may be revised somewhat higher in the updated financial forecast to capture some projects that may have been set aside related to the sale of the utility. As the sale appears unlikely to occur, those expenditures may be incorporated into the upcoming financial forecast. Vero Beach anticipates cash funding for capital expenditures through fiscal 2019.

Great reporting. Maybe now the Wilson,Turner,Heran and others of their ilk will see the light. Thanks Mark for finding this unbiased, non political , report which should put an end to the fake arguments put forth by political operatives like those mentioned above and their friends with ulterior motives.