Editor’s note: Vice-Mayor Harry Howle recently asserted that the sale of Vero Electric to Florida Power and Light will leave the city in a “damn good” position. The following analysis, almost surely beyond Howle attention span, if not over his head, confirms that he, and all those now supporting the sale of Vero Electric, are dead wrong about the supposed financial benefits of the deal. In truth, the sale of Vero Electric will seriously damage the City financially, while yielding only marginal of benefits to the customers of Vero Electric.

Even more damaging that a sale of the full system would be a partial sale, in which the Indian River Shores portion of the system would be carved off and sold to FPL. Tomorrow, InsideVero will publish an analysis of the likely negative impacts of a so-called partial sale.

“Netting the lost fund transfers, franchise fee and net interest income effects, the resulting $4.1MM in net reduction in City revenues may be financed by a combination of (1) increased water utility rates, (2) reduction of General Fund service levels, or (3) increase in ad valorem taxes. (Sale of city assets is not included as a potential revenue source, as suggested, because by definition of prudent financial management practice, non-recurring gains or revenues are never used to fund recurring expense.)”

LEXINGTON

Much adoo about…

Political Analysis

The sale of City of Vero Beach Electric is, and has been for nearly a generation the bitter Third Rail of local politics. If one good things comes from the Full Sale, it will be the end of the poisonous political atmosphere perpetuated in the name of this issue.

Who Benefits?

In the meantime, who benefits from this awful business?

Political careers and organizations and at least one highly-profitable media platform been built on flogging the electric utility.

So it’s much adoo about the activists, their political allies and their dedicated media outlet.

Second, Indian River Shores and South Beach customers will benefit. It is acknowledged that they provide a disproportionate share of the profits reaped by the electric utility. Moreover, it is acknowledged that they cannot vote for the governing body that controls electric policy and rates. These circumstances led a group of them to pool their money to buy an election, and install a City Council that performs to their will.

Their mass-deployment of election capital was greatly magnified by the constant barrage of electioneering propaganda issued from their captive “news” outlet.

It used to be “how you played the game.” Today, the Big Egos get their way by any means. Congratulations – you ‘won.’

Undoubtedly, FPL benefits. They will receive an enormously profitable enterprise.

Given the mark-to-market equity valuation of $64 million as shown below, the system produces about $13.5 in operating cash flow, against which it must spend about $4.0 million to sustain capital investments, leaving $8.5 million in free cash flow.

That’s a return on equity for the City of Vero Beach Electric of 13.3%.

FPL’s regulated return on equity is only 9.6% – 11.6%; Duke Energy earns 6%. Southern Company 11%.

And that’s before the axe comes out to chop down local resources, cut capital spending, cut staff, cut customer service and cut local response. From a reduced cost base–and with political leverage in Tallahassee to enforce continually rising rates, the FPL acquisition will be a goldmine for FPL.

After all, they have put up with – instigated – all the political nonsense and have stuck with it for all these years for a reason – profit.

Corruption

But what’s in it for the We the “Little People” of Vero Beach? Fifty cents a month off your electric bill? A 43% hike in your property tax bill? Is that it—this is all we get?

Unfortunately, no. There’s more: We get corruption.

The Mayor, along with her two council trustys on the City Council, rolled into office on a tidal-wave of special interest money from, you guessed it, FPL.

When asked by a quizzical child, “what is a mayor?” the mayor intuitively responded that it’s “kind of like being Queen.” This moment of honest reflection—shared between a grown-up and an innocent—is apocryphal in explaining the Mayor’s self-image, her imperious style and authoritarian conduct.

Buying an election and a city council to benefit special and sectional interests is extraordinarily bad behavior for those otherwise up-standing citizens of Indian River Shores that donated to “Operation Flip Switch.”

This appalling bullying of the “Little People”—the people who actually live in the City–and their city government has demonstrated to a wider audience that the City Council is up for sale to the highest bidder.

The Mayor and her governing Troika have faithfully represented outside special interests, while willfully neglecting the business and interests of citizens they’re elected and sworn to represent.

Because this has been done in the name of selling the electric utility, it makes it OK?

Consider, instead of the electric utility, a special-interest group intent on building high-rises had bought themselves three seats on City Council. What then? We would all be up in arms.

Notice to outside special interests: all it takes is $150,000 to buy a City Council–chump change for a Miami developer. We have shown them—and they’re watching—that we are a cheap date and you can get your way.

How the Deal Went Down

Starting with the “Letter of Intent,” we were assured that the vote meant nothing as the Letter of Intent was non-binding. It didn’t really commit the City to anything… the terms were not fixed… the City would negotiate on behalf of the citizens from here. Hereinafter, the process would be transparent… the City Council—all of the members—would be afforded an open, transparent and participatory process.

None of it was true. By the next City Council meeting, it became apparent that every one of these promises had been broken.

Does anybody think it’s odd the City did not try to negotiate a higher price? FPL’s initial offer was $185 million – maybe try to get $186, or $187? It may seem like a small amount–$1,000,000—to some people, but why wouldn’t you try?

Doesn’t anybody think it’s odd that the City turned over to FPL—that’s right, FPL—authority to negotiate the City’s exit from deals with OUC and FMPA?

In fact, the Troika decided early on not to even hire a negotiator, which is also odd, except if your plan, from Day-1, was to take whatever FPL offered. In that case, you would not need to hire a negotiator.

We now know that the Letter of Intent was, for all practical purposes, the final deal. The only change was FPL exchanged a portion of the southwest corner of Indian River Boulevard and 17th for one on the northeast corner.

There has been no negotiation. Rather, the Mayor has acted as an ad hoc committee of the City to do substantially all of the work finalizing a contract, out of the Sunshine, and none of this has been done with meaningful participation of the City Council.

All that will be left to City Council will be to rubber-stamp whatever is placed in front of them.

The Mayor has gagged truth-seeking citizen-Commissions, fired the financial advisor, and resisted public calls for a financial plan for the aftermath of the sale.

In other words, there has been a systematic effort to ram through a deal, while hiding from the public what happens starting the day-after they declare “Mission Accomplished.”

Many of our people either don’t know, don’t care and don’t vote. By inaction, by willful ignorance, we have tacitly agreed to be governed as if we were serfs, not citizens. The public tolerates this corruption through inaction.

Voters, please pay closer attention to what’s happening—and not happening—in your city. It belongs to you, not hand-picked, and installed elected officials. Reclaim control of your City. We have a chance to do just that, this November.

Notes and financial analysis…

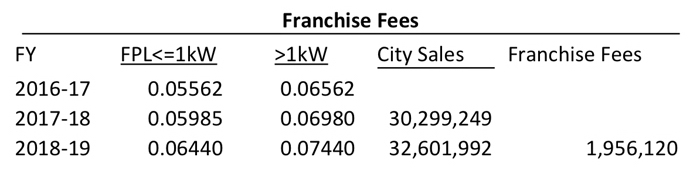

The City has the right to and likely will enact a 6% franchise fee on revenues generated within the City limits by FPL. Applying projected FPL rates to a 2016 baseline as an estimate of consumption, it is estimated that FPL will derive $30,299,249 of sales in the City in 2018, hence the City will receive $1,817,955 in incremental tax revenues.

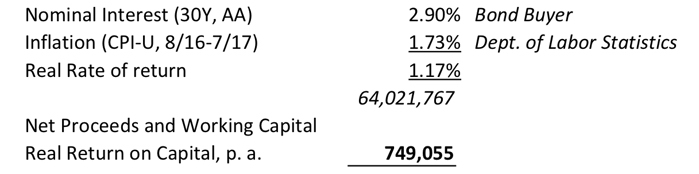

In addition, the City will walk away from the closing table with an estimated $32,000,000, principly due to the liquidation of working capital. As of August 30, 2017, 30-year AA Municipal Bonds yielded 2.90% nominal yield. This approximates the City’s current marginal cost of capital.

That said, the Consumer Price Index Urban, all Items stood at 244.048 in July, 2017, an increase of 1.73% over the prior year period. Hence the inflation-adjusted (“Real” or economic) yield on 30-year AA Muni Bonds was 1.17%.

In order to ensure the purchasing power of future income streams, only inflation-adjusted returns should be considered as “income” subject to distribution. The component of nominal returns attributable to inflation should be retained, and reinvested, as this reinvestment will be necessary to support the future purchasing power of returns.

Therefore, if one expects future inflation to remain at the recent level, the net real interest income attributable to the $32MM principal will be $374,400.

Netting the lost fund transfers, franchise fee and net interest income effects, the resulting $4.1MM in net reduction in City revenues may be financed by a combination of (1) increased water utility rates, (2) reduction of General Fund service levels, or (3) increase in ad valorem taxes. (Sale of city assets is not included as a potential revenue source, as suggested, because by definition of prudent financial management practice, non-recurring gains or revenues are never used to fund recurring expense.)

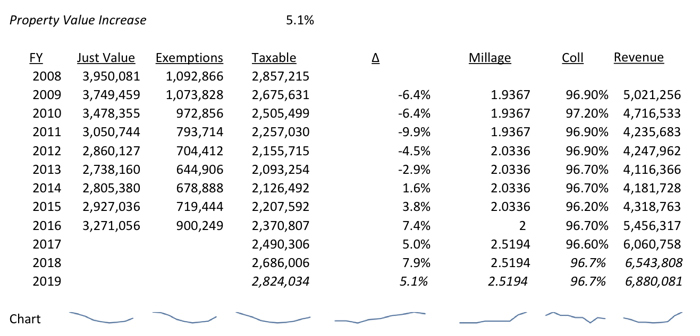

In 2017 the total Tax digest for the City is projected to be 2,686,006,000 and ad valorem tax is budgeted at 2.51940 mills, yielding a projected levy of 6,767,000, 96% of which is collectable.

This amount represents an increase of $500,000 over 2016-17 is principally attributable to rising property values. If this beneficial trend were to continue, it might produce an additional $500,000 in 2018-19, but that is speculative.

All said, for 2018-19, a $4.0 to $4.5MM gap needs to be filled. This equates to a tax increase of 1.50 to 1.67 mills, or an ad valorem tax increase of 60.0% to 66%.

The “typical” constituent (i.e. “voter”) may be thought of as the owner or renter of a median-valued residence. The median-valued property in the City (commercial, industrial, and residential) is $135,880 ($133,514 median for residential only). From the perspective of the property owner (or his renter to whom cost increased will be passed), the pro forma millage increase represents an increase of between $203.82 to $226.91 in annual ad valorem taxes or imputed rent.

For the median taxpayer, this additional tax burden is offset by a projected $6.72 per annum in utility cost reduction due to the change to FPL rates.

FPL Cost Savings Examined

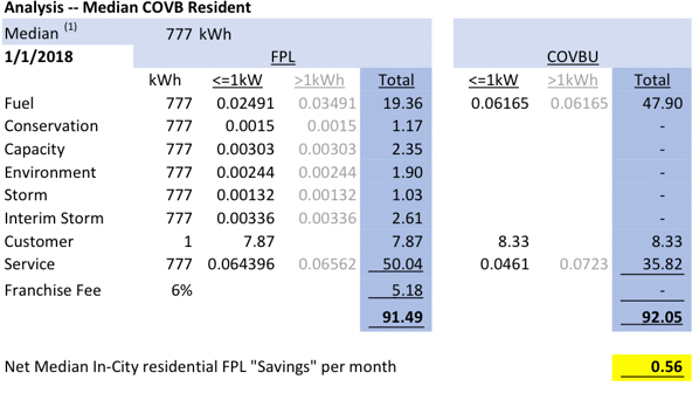

Median Residential Customer

The median customer in the City consumes an average, over a full calendar year, of 777 kilowatt hours (kWh) of energy per month. This figure is calculated from a database of monthly meter readings, for each meter in the system, using the most recent calendar year (2016) as the basis to estimate annual per-household monthly consumption (kWh).

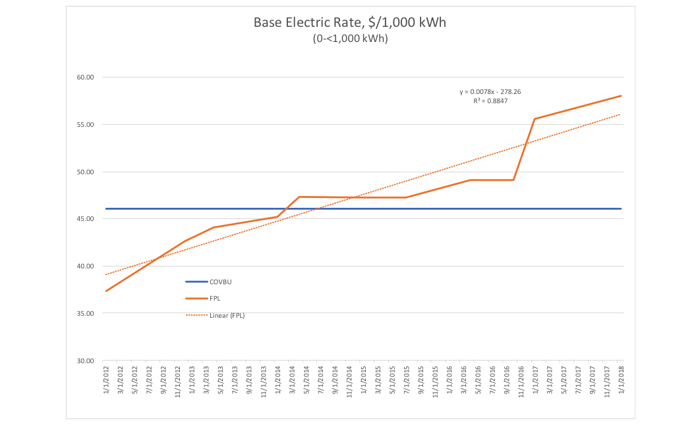

FPL and COVB Electricity Rate history

Tariffs (prices and terms) published by FPL from the period 2012 to present are complied in a database, comprising all classes of customer and service rates offered for a period January 1, 2012 to present.

FPL and COVB Electric Service rates for the period 2012 to present are compared. (Note that the rate charged for electricity service does not include customer charge, fuel, purchased power or other adjustments. ) A forecast based on historical trend is estimated.

FPL Electric Service Cost Trends

While COVB Electric Service rates were flat over the period, FPL’s show a trend of steadily-rising prices. A trendline fitted to monthly-sampled cost data has a coefficient of correlation of 0.94 (R-Squared = 88.47%) indicating a very good fit. The trendline reveals a very steady (0.78% per month – arithmetic average) compound annual growth rate (CAGR) of 7.61%.

The extrapolation of this trend indicates an FPL rate of $64.40/MWh ($0.0644/kWh) by 2019, notwithstanding FPL projections to the contrary based on the 2016 rate agreement. (FPL have a number of ways of raising rates).

Fuel

Fuel and purchased power costs, for FPL and COVB, respectively, are assumed to remain flat for the period of this forecast. To the extent fuel prices fluctuate, it is further observed that changes tend to impact FPL and COVB the same in the short run.

Median Customer Bill Comparison, 1/1/2019

Shortly after the sale transaction takes place and a franchise fee is enacted, FPL’s bill for the median residential customer (777 kWh) is estimated at $91.49 per month, as compared to what would be a COVB Electric Bill of $92.05 – a net difference of 56 cents.

Full Sale Implications for COVB General Fund and Investment Policy Examined

Franchise Fee

The City has the right to and likely will enact a 6% franchise fee on revenues generated within the City limits by FPL. This will be a new revenue source for the General Fund.

It is observed that kWh consumption by residential customers within the City fluctuates seasonally, however there is very little variation and growth is nil year-over-year.

Applying projected 2019 FPL rates to 2016 baseline consumption, it may be estimated that FPL will derive $30,299,249 of sales from all customers in the City in 2018, hence the City will receive $1,817,955 in franchise fees.

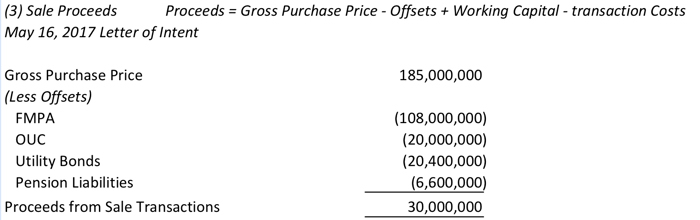

Proceeds from Sale and Liquidation

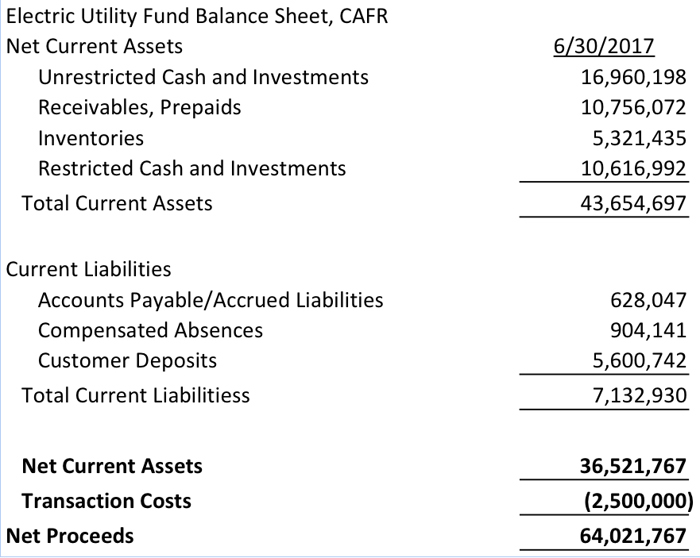

In addition, the City will walk away from the closing table with an estimated $66.5 million:

- From the Letter of Intent , May 16, 2017, the City will net $30 million from the liquidation of the non-current portion of the balance sheet (from FPL).

- In addition, based on 6/30/2017 data, the COVB Electric Fund has $36.5 million in net current assets, contributing to net proceeds of $66.5 million.

Prudential Investment Policy and Sustainable Income

The City should adopt a policy of investment of proceeds and distribution of a portion of the resulting income. Such policy should preserve the purchasing power of the principal as well as that of future income streams. This policy would result in a durable income stream that maintains its purchasing power against general inflation.

To do otherwise would likely result in the steady erosion of the capital asset, and expose the principal to appropriation by future City Councils, without limit. Unfortunately, if left to their own devices, successive City Councils will find it irresistible not to just spend the money.

For this reason, the policy should be given Charter protections, that is, require a public vote to amend or revoke.

Calculation of distributable income

Based on recent trends, an estimate of inflation-adjusted returns may be calculated as:

- Benchmark 30-year AA Municipal Bonds yielded 2.90% nominal yield on August 30, 2017.

- This approximates the City’s current marginal cost of capital.

- Caveats/offsets to market yield:

- Long-dated bonds are highly leveraged to interest rate risk

- Historically-low interest rate environment creates an asymmetric (“heads-I-win-tails-you lose”) risk environment.

- In practice, investment policy would require interest rate risk be mitigated by hedging, laddering or shortening maturities, which would reduce yields.

- The Consumer Price Index, Urban, all Items (CPI-U) stood at 244.048 in July, 2017, an increase of 1.73% over the prior year period. Hence the inflation-adjusted (“Real” or economic) yield on 30-year AA Muni Bonds would be no more than 1.17% (2.90% – 1.73%).

- Given a positively-sloped yield curve, it is unlikely that COVB could outperform this yield throughout the term of this forecast.

- In order to ensure the purchasing power of future income streams, only inflation-adjusted returns should be considered as “income” subject to distribution. The component of nominal returns attributable to inflation should be retained, and reinvested, as this reinvestment will be necessary to preserve future purchasing power of future income.

Figure 7 – Estimate of sustainable returns from risk-appropriate investment position. It has been alternatively suggested that the City could invest proceeds from the Full Sale along the lines of a “Hedge Fund,” that is, investing for yield and growth in both debt and equity securities, with the addition of borrowed funds to effect leverage.

The legality or appropriateness of this approach is debatable, to say the least, and well beyond the scope of this forecast.

All told, distributable income from $66.5MM principal is estimated at $749,055 per annum.

Ad Valorem Taxes

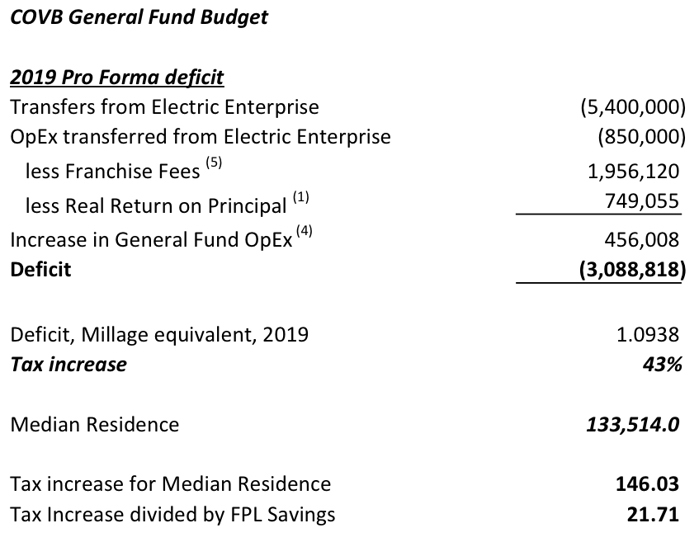

Netting the lost fund transfers, franchise fee and net interest income effects, the resulting $3.1MM in net reduction in City revenues may be financed by a combination of (1) increased water utility rates, (2) reduction of General Fund service levels, or (3) increase in ad valorem taxes.

(Sale of city assets is not included as a potential revenue source, as suggested, because by definition of prudent financial management practice, non-recurring gains or revenues are never used to fund recurring expense.)

- In 2017-18 the total Tax digest for the City is projected to be 2,686,006,000 and ad valorem tax is budgeted at 2.51940 mills, yielding a projected levy of 6,543,808 with a 96.7% collection rate.

- This amount represents an increase of $483 thousand over 2016-17 is principally attributable to rising property values.

- If the beneficial trend in real estate values of the past five years were to continue, it would produce an additional $336 thousand in 2018-19.

4. However, General Fund expense will also likely rise in 2018-19. Given recent historical trends, if the City is very conservative, this might be held to the previous year’s increase—which approximates the rate of inflation over the period—of 1.9%.

5. All said, for 2018-19, a $3.1 million gap needs to be filled. This equates to a tax increase estimated at 1.09 mills, or an ad valorem tax increase of 43%.

From the Point of View of the “Median household…”

The “typical” resident may be thought of as an occupant of a median-valued residence. In addition, the typical residential household is, approximately, a median-valued electric utility customer.

- The City’s median property value (commercial, industrial, and residential) is $135,880 (IRC Tax Appraiser database, 8/17/2017 version);

- The median residence (IRC Tax Appraiser Property-Use Codes 01, 04) is valued for tax assessment purposes at $133,514.

From the perspective of the resident (owner or renter to whom cost increased will be passed), a 1.0938 millage increase needed to balance the City General Fund in 2019 represents an increase of $146 in annual ad valorem taxes or imputed rent—a figure that is more than 20 times the projected FPL savings for that same median household.

Here is how I compare this all out fiasco to a class of third graders voting on a class president:

The choice for a class president was narrowed down to two.

The first candidate got up and spoke about how he would make the class a better place. He ended his speech by promising to do his very best.

The second candidate got up and said, “I will give you free ice cream” and sat down.

The class went wild. “Yes, yes!!! We want free ice cream!”

A discussion followed. How will they pay for the ice cream? The candidate wasn’t sure. Would her parents buy it or would the class pay for it? The candidate didn’t know.

The class didn’t care. All they were thinking about was free ice cream.

The first candidate was forgotten. All the class was thinking about was free ice cream.

Every time Moss, Howle and Sykes opened their mouth, they promised free ice cream, and 51% of Vero Beach acted like nine year olds.

They wanted ice cream.

The other 49% of the citizens of Vero know they’re going to have to feed the cow and clean up the mess.